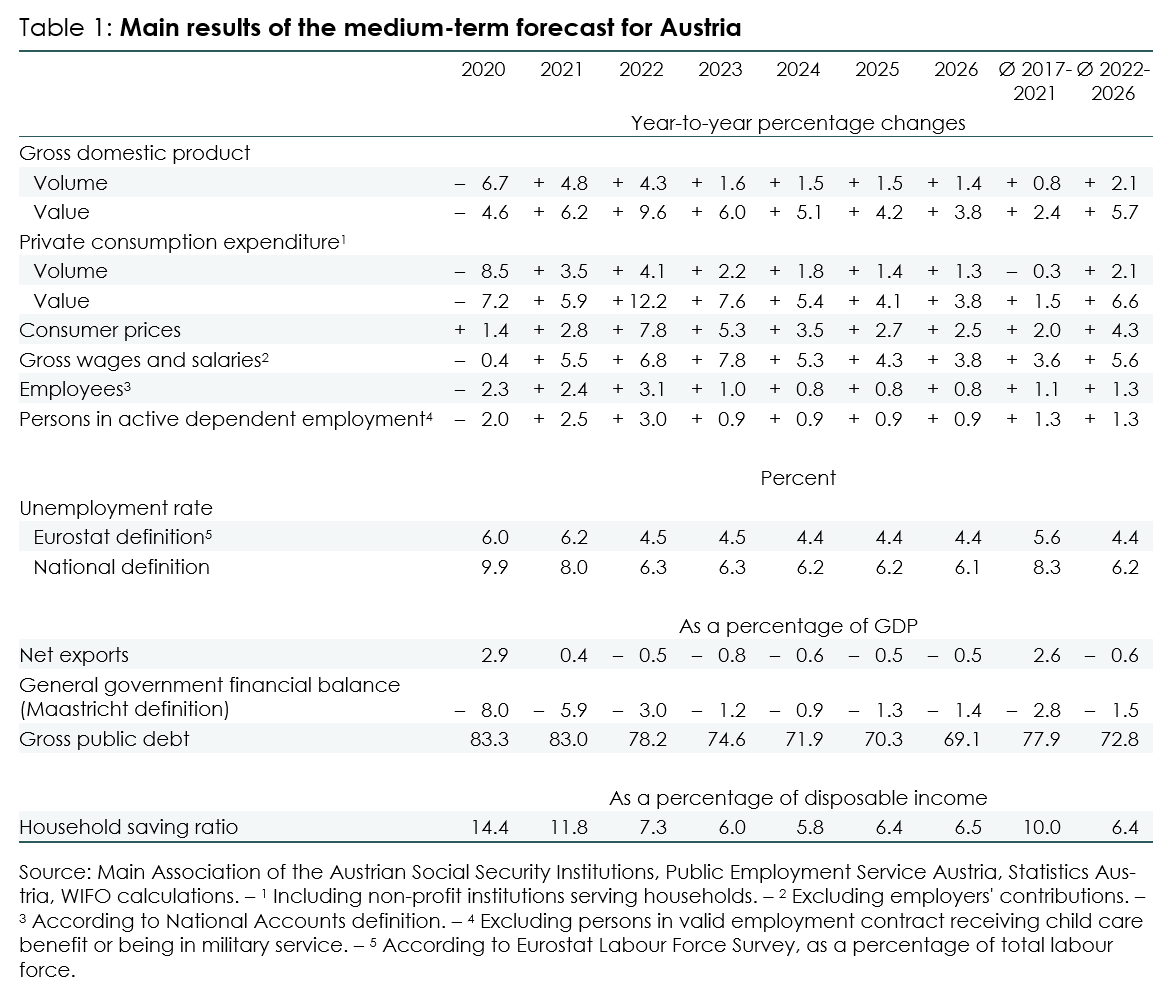

Due to the strong economic growth in the first half of the year, which is attributable to considerable base and carryover effects, economic growth of 4.3 percent is still expected for 2022. As a result of the Ukraine war and the COVID-19 pandemic, growth prospects weaken markedly from the second half of the year, and GDP growth of only 1.6 percent is estimated for 2023 (–0.4 percentage point compared to WIFO's Economic Outlook of March 2022). By the end of the forecast horizon, an average economic growth of 1.5 percent per year is expected.

The war in Ukraine and the COVID-19 pandemic are massively amplifying and prolonging the strong upward price trend already observed globally since 2021. This is mainly driven by sharp rises in energy, raw material, and intermediate product prices as well as a significant increase in transport costs due to capacity constraints and the resulting delivery delays. In addition, the grain shortage caused by the Ukraine war on the world market and increased production costs (fuel, fertilizer) are causing sharp rises in food prices. In Austria, consumer prices are expected to rise by nearly 8 percent in 2022 and by 5.3 percent in 2023. By the end of the forecast horizon, inflation is expected to decline to 2.5 percent. Inflation is thus expected to remain above the ECB's inflation target over the entire forecast period.

Real per capita wages are set to fall very significantly by almost 4 percent in 2022 due to high inflation. In particular, due to the delay in wage indexation by around one year and the fall of inflation over the forecast period, real wages are expected to increase by 1.3 percent to 0.5 percent p.a. from 2023 to 2026, although with a downward tendency. However, these increases are well above the average real wage increase of +0.2 percent p.a. in the between-crisis period of 2010-2019. For nominal gross wages and salaries sum, the evolution of employment, real wages per capita and inflation results in a declining growth from 7.8 percent (2023) to +3.8 percent in 2026.

The forecast takes into account the implementation of the 2022-2024 eco-social tax reform on 1 January 2022, three packages of measures to dampen the erosion of purchasing power caused by high inflation, and additional spending to take care of refugees from Ukraine. In addition, a significant tightening of monetary policy is assumed, causing long-term interest rates in Austria to reach a level of 4.5 percent from the middle of the forecast period – 3 percentage points higher than assumed in the March forecast. As a consequence, public debt interest service will increase more markedly.

As a result of lower public sector revenues and higher public spending, the budget deficit in 2022 will be 3 percent of nominal GDP, a more than half percentage point higher than expected in March. Due to the compensation of the tax bracket effects from 2023 onwards, the revenue shortfalls will cumulate. At the end of the forecast period, a deficit ratio of 1.4 percent (+1 percentage point compared with the WIFO Economic Outlook of March 2022) and a government debt ratio of 69 percent are expected.

Risk assessment

In this medium-term forecast, no further significant restrictions on economic activity due to the COVID-19 pandemic were assumed for Austria and its most important trading partners (e.g., China) from the second half of 2022. Furthermore, it was assumed that natural gas and crude oil supplies from Russia and Kazakhstan, respectively, will not be permanently constricted.

The COVID-19 pandemic and, in particular, the Ukraine war entail significant downside risks for the first years of the forecast. The emergence of new, more dangerous variants of the SARS-CoV-2 virus, in particular those against which the vaccines currently available do not offer any protection, could again lead to lockdowns and supply bottlenecks in the fall of 2022 and early 2023 and significantly dampen economic activity.A further escalation of the Ukraine war could lead to supply restrictions for crude oil and natural gas and/or to an expansion of the EU sanctions on Russian energy raw materials. In the event of a natural gas supply freeze or embargo, the European economy would slide into recession. If Russia were to permanently hinder or stop crude oil deliveries from Kazakhstan to Austria, this would make crude oil supplies more expensive. At the same time, inflation would turn out to be higher than assumed in the forecast.

Russia's share in the overall natural gas imports is significantly higher in Austria than e.g., in Germany (2021: Austria 86 percent, Germany almost 40 percent). For a landlocked country that is more dependent on pipeline supplies, it is more difficult to compensate delivery shortfalls by other sources of supply. Replacing natural gas with other forms of energy inputs is also more difficult in Austria since the electricity generated in gas-fired power plants can hardly be replaced by coal-fired power plants and not at all by nuclear power plants. Thus, in the event of a natural gas supply shutdown, the domestic energy intensive industry and electricity and district-heat generation are likely to be hit by a more severe economic decline than in Germany.

As the war will continue, destruction will increase, and civilian atrocities will continue, the number of people from Ukraine seeking shelter in the EU will also increase. An escalation of tensions in the Middle East or between Turkey and the EU could also reinforce other migration flows to Europe and increase the challenges in providing care and integrating refugees.

If the mentioned downside risks materialize, Austrian exports would develop weaker and input cost will be higher than assumed in the forecast. Economic growth, employment, and income development as well as tax revenue in Austria would be weaker, while government spending would tend to be higher than assumed.

For the period 2022 and 2023, this medium-term forecast is based on the WIFO Economic Outlook presented on 30 June 2022 ("summer forecast") and was extrapolated to 2026 using the econometric model WIFO Macromod under assumptions made for the international economy and domestic and EU economic policy.